You are currently browsing the tag archive for the ‘economics’ tag.

Consider a team selling tickets for its upcoming baseball season. Before the season begins it offers a bundle of tickets for every game. Some of these games however are certain to have very low attendance (games on a Tuesday, games against poor opponents, etc.) The tickets for these games will be placed on the secondary market at very low prices. Indeed one of the biggest problems for teams is the inability to prevent those secondary market prices from falling so low that they cannibalize single-game box office sales. The problem is so severe that many baseball teams are making arrangements with StubHub to enforce a price floor on that exchange.

The problem has a much simpler solution: stop selling season tickets. The team should instead offer the following type of bundle: you may purchase tickets for all of the predictably high-demand games at the usual season ticket discount.Then you may add to that bundle any subset of the low-demand games you desire but each at a price equal to the face value of the ticket.

This arrangement will make both season ticket holders and the team better off. Season ticket holders will opt not to add the low demand games (unless the opponent is a team they really like for example) and since they weren’t going to those games anyway they are saving money.

The team will increase revenue: supply of tickets to low demand games will be controlled. Secondary market tickets will be priced at or near face value because nobody will buy a ticket at face value for a lousy game unless they actually plan to use the tickets. This enables the team to hold prices at their desired (i.e. revenue maximizing) level without cannibalism.

We, Jeff and Sandeep, are working with Northwestern Sports to launch what we think is going to be a revolutionary way to sell tickets to sporting events (and someday theatre, concerts, and restaurants…). Starting today it is in effect for two upcoming Mens’ Basketball games: The February 28 game against Ohio State and the March 7 game against Penn State.

We are using a system which could roughly be described as a uniform price multi-unit Dutch Auction. In simpler terms we are setting an initial price and allowing prices to gradually fall until either the game sells out or we hit our target price. Thus we are implementing a form of dynamic pricing but unlike most systems used by other venues our prices are determined by demand not by some mysterious algorithm.

But here is the key feature of our pricing system: as prices fall, you are guaranteed to pay the lowest price you could have got by delaying your purchase. That is, regardless of what price is listed at the time you reserve your seat, the price you will actually pay is the final price.

What that means is that fans have no reason to wait around and watch the price changes and try to time their purchases to get the best possible deal. We take care of that for you.

It also removes another common gripe with dynamic pricing, different people paying different prices for the same seats. Our system is fair: since everyone pays the lowest price, everyone will be paying the same price.

We explain all of the details in the video below. If you have any questions please ask them in the comments and we will try to answer them.

The system is live right now at NUSports.com. Support common-sense pricing by heading over there now and getting your tickets for either NU v Ohio State on Feb 28 or NU v Penn State on March 7.

And Go ‘Cats!

Update: Price alerts are now available. You may send email to wildcatmarketing@northwestern.edu to be notified when prices fall. (And if you just want to know when prices reach some target p, put that in your message.)

The paper doesn’t seem to exist yet but here are slides from talk by Raj Chetty, Emmanual Saez and Lazlo Sander. They randomly altered the incentives for referees at the Journal of Public Economics to see what it takes to get referees to give timely reports. Some referees were offered cash. Some were simply given shorter deadlines with no carrots. Still others were threatened with public shame if they did not submit reports on time. Not surprisingly the threat of humiliation caused many referees to refuse the contract altogether. Perhaps less surprisingly, cash didn’t do much better than simply shortening the deadline. The latter did help a bit.

Kofia krumple: Tobias Schmidt

- When you turn a bottle over to pour out its contents it is less messy if you do the tilt thing to make sure there is a space for air to flow back into the bottle. But which way of pouring is faster if you just want to dump it out in the shortest time possible? I think the tilt can never be as fast.

- I aspire to hit for the cycle: publish in all the top 5 economics journals. But it would be a lifetime cycle. Has anyone ever hit for the cycle in a single year?

- If you know you’ll get over it eventually shouldn’t you be over it now? And if not should you really get over it later?

- The efficient markets hypothesis means that there is no trading strategy that consistently loses money. (Because if there were then the negative of that strategy would consistently make a profit.) So trade with abandon!

- I predict that in the future the distinct meanings of the prepositions “in” and “on” will progressively blur because of mobile phone typos.

Drawing: Scatterbrained from www.f1me.net (yaaay she’s back.)

That commercial was rejected for the Super Bowl broadcast yesterday. And because of that it will be seen by many many people (even you!). Indeed the value of the publicity from being rejected rivals that of being accepted. You’ll get people actively watching your ad rather than just passively.

This is a problem for the broadcaster because first of all it is failing to capitalize on a valuable asset: the monopoly authority to reject ads. Second the plethora of rejected ads and their publicity dilutes the value of its other asset: the monopoly provider of broadcast airtime. So the Super Bowl broadcast network needs to find a way to capitalize on the publicity they can generate by rejecting ads and also to make rejected advertisers pay for the negative externality on accepted advertisers. How to do it?

Charge an enormous price to submit your ad for consideration. If you are accepted you get the submission fee refunded. If you are rejected, tough luck.

Added: You can also put a check box on the submission form allowing advertisers to secretly specify whether they want to be accepted or rejected.

Some might prefer the publicity/price of rejection over the actual broadcast. Without the checkbox they might not submit out of fear they will be accepted.

Imagine the publicity you can get when a marginal ad (like the one above) is rejected “unfairly.”

I say the deadweight loss here is not so large. Most art exhibitions are not self-financing from the side of the viewers, which suggests that the demand to see the pictures is not higher than the costs of mounting the exhibit. Arguably you can throw in philanthropic support as another part of “market demand,” but I consider that a separate valuation issue. Maybe our current artistic institutions are under-providing marketing opportunities for businesses and foundations, but that still won’t get you a major pent-up demand to view the pictures, again not relative to cost. The very popular pictures, such as the good works by the Impressionists and post-Impressionists, are shown quite frequently, including in traveling exhibitions.

Context matters a great deal in this setting. Currently most of the Louvre is not being viewed at any point in time, as the crowds tend to cluster in a few very well-known areas. Many people would want to go see anything they are told they ought to go see. What is underfunded is some kind of “demand for participation in a public event,” not the viewing of art per se. If only they could create more hullaballoo around the more obscure Flemish painters.

Almost all museums have large stretches of empty walls. I would put up many more pictures there, as indeed I do in my own home. That museums do not do this I find striking and indicative. Nor do I see viewers and visitors demanding this, if anything the unspoken feeling might be to wish for a bit less on the walls, so that one may have the feeling of having seen everything without exhaustion.

The costs of storing art are high. Perhaps the Louvre should sell some of its lower-tier works to private collectors. But the general public just doesn’t want so much more art to see, not if they have to pay for it and maybe even if they don’t.

Nice.

But I can’t help but ask what was the deadweight loss of all of Tyler’s ideas lost to the world pre-blogosphere? Is MR self-financing? How good a measure is the price (free) of the consumers’ surplus it generates now?

I just hope this doesn’t make me a Flemish painter.

Check out the prices on Stub Hub for tickets to the upcoming Big10 basketball game between the Iowa Hawkeyes and the Wisconsin Badgers. Quite a few of them are significantly below the $24 face value of the tickets. This can happen because fans who buy season tickets for Badgers basketball are buying for the games against the conference powerhouses. For the games against cellar dwellers like Iowa they dump their tickets on the secondary market at whatever price they will fetch.

Coping with scalpers who buy tickets through the box office and resell them at inflated prices is one thing. You could have raised prices yourself but you chose not to. But what do you do when scalpers are undercutting your box office price?

You should buy the tickets back from the scalpers is what you should do. The fans who are going to buy from the scalper at the low price might also be willing to buy at box office prices. If you buy the cheap tickets on StubHub first then the box office is the only option left for them. And if they do buy from the box office you have made a profit because you bought low and sold high.

But there’s a chance those fans aren’t willing to pay box office prices and in that case you’re just losing money. So there’s a tradeoff. It means that you don’t want to buy secondary market tickets at prices just below your box office price but you definitely do want to buy the tickets priced so low that they are worth the risk. Indeed there is some optimal offer price that you should be prepared to repurchase tickets at.

In fact every venue’s box office should be both a buyer and seller of tickets with an optimally calculated spread between bid and ask prices.

Now you might wonder whether this only further encourages season ticket holders to dump their unwanted tickets. Indeed it does but that’s exactly what you want them to do. The tickets will be reallocated more efficiently and you will capture the gains from trade. Moreover, fans are now willing to pay higher prices for season tickets if they know they can easily resell their unwanted tickets. You can then raise season ticket prices to capture those gains.

Free as in liberated. Here’s the opening paragraph:

I wrote this paper with the recognition that it is unlikely to be accepted for publication. There is something liberating about writing a paper without trying to please referees and without having to take into consideration the various protocols and conventions imposed on researchers in experimental economics (see Rubinstein (2001)). It gives one a feeling of real academic freedom!

The paper reports on long-running experiments relating response times to mistakes in decision-making.

Its here. I like the purpose, as given on the masthead:

This blog is to help me remember stories and papers and provide ideas for students taking the Behavioral and Experimental class. It will focus on behavioral and experimental economics, with the occasional gender story.

Most of the posts are indeed links to papers with quotes from abstracts, but I enjoyed this one departure from normal programming

One of my colleagues talked about a (not very inspired) way to do research, which he adequately describes as keyword research (and which he denounces whole heartily). The idea is the following, which seems to work very well for theory papers: Take a bunch of keywords, select a few, check if a paper has been written if so, try again…

In that spirit, I came across the following blogpost: Sociology title Generator

Bearskin bow: Mobius.

Its called Nostra Culpa and its a 16 minute 2 act opera dramatizing the exchange on Twitter between Paul Krugman and Estonian President Toomas Ilves about that country’s austerity program. Robert Siegel interviewed the librettist and composer on NPR yesterday:

SIEGEL: I would sort of have expected you to have written this for a tenor and a baritone. But unexpectedly, for me at least, the two characters – Paul Krugman and President Ilves of Estonia – are both sung by the same mezzo-soprano.

BIRMAN: Right. Well, the mezzo-soprano is somebody I’ve worked with before and she’s, I think, one of the greatest talents in Estonia as a dramatic singer. And my idea – my sort of inspiration to set these words was not so much to make some kind of argument, but to have the singer portray the people themselves who are stuck in this – between these two sides.

SIEGEL: Now, one writer observed that the entire exchange between Krugman and Ilves consisted of a 70-word blog post with chart, and then four tweets. Puccini had a lot more to work with when he sat down to write “Tosca,” let’s say.

BIRMAN: Well, one could write an opera, a full-length two-hour opera, using just this content, in my opinion. Because, in a way, why is the story interesting? To me it’s interesting because we have been discussing this ever since 2008, 2009 – what to do and how to get out of this, and we’re still not out. And the story is being written as we go.

The opera has its debut on April 7 in Estonia.

Consider a monopolist which sells two different goods to two independent markets. The firm sets the profit maximizing price in the two separate markets and suppose one of those prices is high and the other is low. Now suppose the firm bundles the two goods: they are no longer sold separately but instead if you want one you must buy both. The profit-maximizing price of the bundle will be higher than the low priced good but lower than the high priced good. Consumers of the previously low-priced good are worse off, consumers of the previously high-priced good are better off because of the bundling.

This is one simple point to have in mind when thinking about bundling of cable channels versus a la carte pricing. The bundling mixes the elasticities of the two separate demand curves and leads to pricing in between the individual profit-maximizing prices. If sports channels are in high demand and food channels are in low demand then people who like food but not sports are justified in complaining about bundling.

But as Alex Tabarrok points out, these complaints are often poorly targeted, instead focusing on the differential costs cable networks charge the cable companies for access. Bundling is often viewed as a way of cross-subsidizing high-cost cable channels by raising prices on subscribers who view low-cost channels. For example Kevin Drum, responding to an article in the LA Times breaking down the cable companies’ balance sheets, asks for a la carte pricing so that

“sports fans would be forced to pay the actual cost of their sports programming without being subsidized by the rest of us.”

Alex presents a simple example to demonstrate that this focus on costs is misguided. But just because they’ve got their reasoning wrong doesn’t mean they came to the wrong conclusion. And in debunking the analysis Alex himself overlooks the basic point about bundling above.

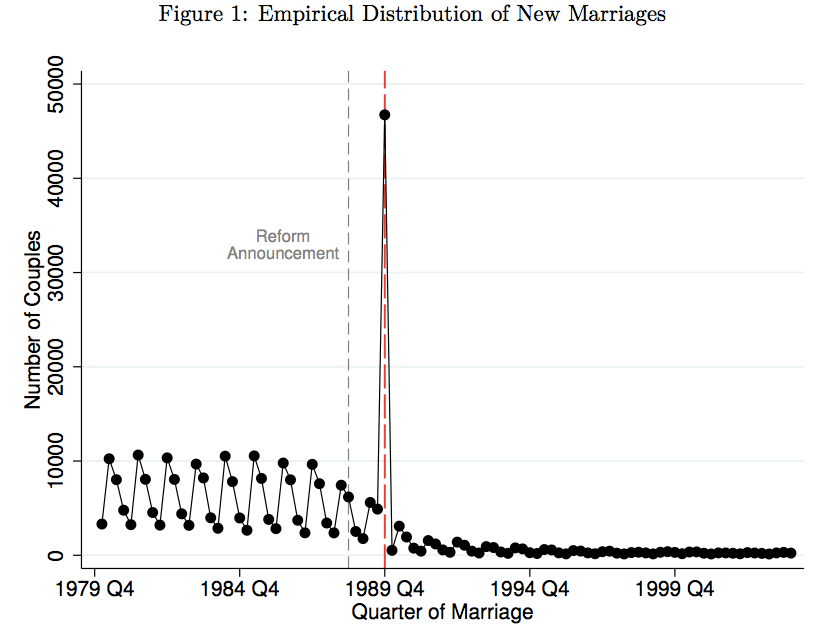

In June of 1988 in Sweden it was announced that survivorship benefits, a sort of government provided life insurance paid to a wife whose husband dies, would be discontinued. There was one interesting exception: an unmarried couple with a child together born before the change could take up survivorship insurance if they married before Jan 1 1990. The spike in new marriages in the graph shows the response to this incentive.

That’s the basis for Petra Persson‘s job market paper. Petra points out that the spike is somewhat mysterious because for all of these couples the promise of survivorship insurance wasn’t enough to induce them to marry previously and only when the option was going to disappear did they exercise it.

Of course some of these new marriages were couples that planned eventually to marry (and take up benefits) and who moved their marriage date earlier. But Petra credibly demonstrates that a large proportion of these marriages were marriages that never would have happened had the reform not been announced. What explains those “extra” marriages?

Petra’s theory is that these couples were still uncertain about whether they were a good match and were planning to live together longer before deciding later whether to marry. After the reform was announced this option to wait and see was no longer costless and therefore many of these couples rushed into a marriage that, given enough time, they might have eventually decided against.

There’s an alternative story that fits equally well. Consider a couple where there is no uncertainty at all about whether the match is good: its a bad match and that’s why they are not married. (Or it could be that they are perfectly happy together but just see no value in being legally wed.) This couple optimally plans to wait until the husband is close to death and then (if he hasn’t married somebody else) get married in order to take up survivorship insurance. Now once the reform is announced that option is removed and they re-optimize and marry December 31, 1989. Many of these are extra marriages because if they waited he might die unexpectedly or marry somebody else.

This theory (like Petra’s) also explains some other facts. For example, conditional on the husband not dying shortly after the reform the divorce rate for these marriages was unusually high. And even after controlling for everything a private insurance company would use to assess risk, takeup of the survivorship insurance via marriage is a good predictor of earlier-than-expected death.

I wonder what we could look for in the data to distinguish the two theories.

It’s a great paper and there’s lots more in there, you should definitely take a look. If I were making a list this year (I am not) Petra would definitely be on it. (Check out her paper on information overload.)

Here’s what I presented on Friday in Cambridge:

And here’s what I presented on Saturday in Chicago:

From the blog of The Socialist Party of Great Britain, via Markus Mobius:

What Shapley and Roth had in fact worked on was how to allocate resources to needs in a non-market context. As the Times went on to say, they worked out in theory (Shapley) and practice (Roth) how to match ‘doctors to hospitals, students to dorm rooms and organs to transplant patients,’ adding ‘such matching arrangements are essential in most Western countries where organ-selling is illegal, and the free market cannot do the normal work of resource allocation’ (like allocating organs to those who can pay the most).

And this:

So, we really are talking about a non-market way of allocating resources. As socialism will be a non-market society where the price mechanism won’t apply to anything, the winners’ research will be able to be used for certain purposes even after the end of capitalism; which is not something that can be said of the work of most winners of the Nobel Prize for Economics.

No doubt it would continue to be used to allocate organs to transplant patients and students to rooms. In fact, this last could be extended to allocating housing to people living in a particular area. While they may not get their first choice, people would get something for which they had expressed some preference and that corresponded to their needs and circumstances. It might even help answer Bernard Shaw’s question, ‘Who will live on Richmond Hill in socialism?’ Since socialism will be a non-market society the answer can’t be, as it is under capitalism today, ‘those who want to and who can afford to.’ This would not only be ‘repugnant’ but impossible.

From the blog (?) notes.unwieldy.net:

The average New York City taxi cab driver makes $90,747 in revenue per year. There are roughly 13,267 cabs in the city. In 2007, NYC forced cab drivers to begin taking credit cards, which involved installing a touch screen system for payment.

During payment, the user is presented with three default buttons for tipping: 20%, 25%, and 30%. When cabs were cash only, the average tip was roughly 10%. After the introduction of this system, the tip percentage jumped to 22%.

He calculates that the tip nudge increased cab revenues by $144,146,165 per year.

By Ivo Welch. Here is the abstract:

This paper analyzes referee recommendations in two settings: The first setting is a prestigious finance conference, in which a computer algorithm matched referees to papers based only on shared expertise. The second setting is the standard journal process, with data from eight prominent economics and finance journals (ECMTA, JEEA, JET, QJE, IER, RAND, JF, RFS). Despite referee selection differences, the data suggest similar referee behavior in both settings. First, referees display only modest consensus. Second, referees disagree not only about scales (a referee mean effect), but also about the relative ordering of papers. Third, the bias measured by the average generosity of the referee on other papers is about as important in predicting a referee’s recommendation as the opinion of another referee on the same paper.

In sum, the typical referee report consists roughly of one part signal of some referee- agreeable objective attribute of the paper and two parts (referee-specific) noise. In turn, the noise itself consists roughly of one part referee-mean effect (bias) and two parts unidentified effects or noise.

The random selection of referees removes this potential objection.

The self-correcting ticket price.

It’s clear that lots of sports franchises suffer from suboptimal ticket-pricing schemes. Between games that feature many empty seats, games that sell out entirely, and the ability of scalpers to obtain profits on the secondary market, money is obviously being left on the table. The University of Minnesota is trying an interesting idea with its new Golden Ticket pricing concept that for $75 lets you attend all nine Big Ten men’s basketball matchups.

But with a catch.

The catch is that if you go to a game and Minnesota loses, then your pass expires.

The idea is that demand is low for games against weak opponents so Golden Ticket holders will fill the empty seats. They will find it too risky to attend the games against strong opponents freeing up supply to accomodate the increased demand for those games.

Coonskin curl: Mark Witte.

- To indirectly find out what a person of the opposite sex thinks of her/himself ask what she thinks are the big differences between men and women.

- Letters of recommendation usually exaggerate the quality of the candidate but writers can only bring themselves to go so far. To get extra mileage try phrases like “he’s great, if not outstanding” and hope that its understood as “he’s great, maybe even outstanding” when what you really mean is “he’s not outstanding, just great.”

- In chess, kids are taught never to move a piece twice in the opening. This is a clear sunk cost fallacy.

- I remember hearing that numerals are base 10 because we have 10 fingers. But then why is music (probably more primitive than numerals) counted mostly in fours?

- “Loss aversion” is a dumb terminology. At least risk aversion means something: you can be either risk averse or risk loving. Who likes losses?

All working for tech companies and all profiled in this article in The Economist.

ON THE face of it, economics has had a dreadful decade: it offered no prediction of the subprime or euro crises, and only bitter arguments over how to solve them. But alongside these failures, a small group of the world’s top microeconomists are quietly revolutionising the discipline. Working for big technology firms such as Google, Microsoft and eBay, they are changing the way business decisions are made and markets work.

A monopolist considers whether to disclose some information about its product. The information will affect how the consumer values the product but its impossible to predict in advance how the consumer will react. With probability q the consumer will view it as good news and he would be willing to pay a high price V for the product. But with probability 1-q it will be viewed as bad news and the consumer would only be willing to pay a low price v where 0 < v < V.

The consumer’s reaction to the information is subjective and cannot be observed by the monopolist. That is, after disclosing the information, the monopolist can’t tell whether the consumer’s willingness to pay has risen to V or fallen to v.

In the absence of disclosure, the consumer is uncertain whether his the value is V or v and so his willingness to pay is equal to the expected value of the product, i.e. qV + (1-q)v. This is therefore the price the monopolist can earn.

Supposing that the monopolist can costlessly disclose the information, what would its profits be then? It won’t continue to charge the same price. Because with probability (1-q) the consumer’s willingness to pay has dropped to v and he would refuse to buy at a price of qV +(1-q)v. At that price he will buy only with probability q and since that would be true at any price up to V, the monopolist would do better setting a price of V and earning expected profit qV.

Alternatively he could set a price of v. For sure the consumer would agree to that price (whether his willingness to pay is V or v) and so profits will be v. And since this is the highest price that would be agreed to for sure, v and V are the only prices the monopoly would consider. The choice will depend on which is larger qV or v.

But note that both qV and v are smaller than qV +(1-q)v. Disclosing information lowers monopoly profits and so the information will be kept hidden.

This little model can play a role in the debate about mandatory calorie labeling.

The remaining videos for my Intermediate Microeconomics course have been uploaded for your viewing pleasure. Here’s a sample, and the rest are all at the link.

A new paper by Lionel Page and David Savage. The abstract:

This study explores people’s risk attitudes after having suffered large real-world losses following a natural disaster. Using the margins of the 2011 Australian floods (Brisbane) as a natural experimental setting, we find that homeowners who were victims of the floods and face large losses in property values are 50% more likely to opt for a risky gamble – a scratch card giving a small chance of a large gain ($500,000) – than for a sure amount of comparable value ($10). This finding is consistent with prospect theory predictions of the adoption of a risk-seeking attitude after a loss.

There is a stockpile of bottled water over here and a bunch of thirsty people over there. What should be done?

Before you can answer that question you first have to figure out what is possible. Don’t think yet about what institution or economic system you are going to use to bring about the outcome, first just ask what is feasible in principle.

There are two choices to make. First, which consumers will get water bottles (the allocation). And second, how much money will be transferred from the consumers to the suppliers (the transfers).

The welfare associated with any choice can be summarized by a pair of numbers: the total utility or surplus of consumers and the surplus of producers. You can plot the set of all such pairs that can be generated by some choice of allocation and transfers on a graph where consumer surplus is on one axis and producer surplus is on the other.

We are really interested in the Pareto efficient choices: the ones on the frontier of the feasible set. In our problem the frontier is a line with slope negative 1. Here’s how you achieve these points. First you allocate all of the water bottles to those consumers who value them the most. This achieves the maximum total surplus. Then you specify transfers in order to distribute this surplus in various ways between suppliers and consumers. As you vary the transfers you move along the frontier swapping producer for consumer surplus dollar for dollar.

Now that you have the feasible set you ask yourself what your social welfare function is. That is, how do you compare different points on the graph? You are essentially saying how you evaluate tradeoffs which reduce the utility of one individual and raise the utility of another. Once you have settled on a standard you choose the best point from the frontier according to that standard.

Then you start asking what economic system you can use to achieve it.

The price system is one. But the price system has a big problem. When water bottles are allocated by setting a price the two dimensions in your graph collapse into one. For example, if you want to achieve the surplus maximizing allocation with a price you are forced to accept one particular division of that surplus. There is a market clearing price p and every consumer who gets a bottle of water pays p to a supplier.

Another way of saying this is that market clearing prices correspond to one single point on your frontier. Is it the point you wanted before you started considering the price system as a mechanism? That would be quite an accident. And barring such a coincidence you are now left asking what else could be done within the confines of the price system?

You can choose a price different from the market clearing price. As you vary the price you do two things. First, you worsen the allocation and as a result total surplus goes down. So you move inside the old frontier. That’s bad. Second, you change the division of surplus. This traces out a new frontier giving you more than one choice. That’s good.

Now you can consult your social welfare function again and ask which point on the price-system-generated frontier do you like the best. Will it be the point corresponding to market-clearing prices? Of course it depends on your social welfare function but again it would be quite a coincidence.

For example it could be that market-clearing prices are very high and give almost all surplus to producers and leave consumers with close to zero surplus. If your social welfare function has diminishing marginal rate of substitution of one individual’s utility for another (whether they are consumers or producers, it doesn’t really matter) you will prefer a more interior point which would be achieved by setting prices below market-clearing levels. You are essentially willing to reduce total surplus by a bit (due to misallocation) in order to achieve a better distribution.

Thus, my response to Erik Brynjolffson, who writes in the comments to my post on price gouging:

Producers also are people, just like consumers, and we’d like to see their utility increased, ceteris paribus. Thus, even if production decisions don’t change, I don’t follow your argument that we should put zero weight on producer surplus.

is that nowhen did I say that we should do that and it’s not part of the argument. Instead the argument is that as long as you don’t think we should always be indifferent to arbitrarily reducing the surplus of one party in favor of another (again regardless of who is a consumer or a supplier) then your optimal price will not be the market-clearing price.

Let me emphasize that this is a very special problem because the quantity of water bottles was given, we don’t have to worry about incentives to produce. Another effect of the price system is to provide those incentives. And when supply is elastic, distorting prices reduces welfare for another reason: the quantity is distorted. The point I am making applies in the special cases when this distortion is small. For example when supply lines are cut in a natural disaster.

Other commenters, like Tyler Cowen, argue that supply cannot be considered perfectly inelastic even in rare, unexpected natural disasters. That’s true, but this is not a limiting argument. It doesn’t require perfectly inelastic supply. The tradeoff is still there with highly, but not perfectly, inelastic supply.

Eli Dourado wrote this on Twitter:

Despair. RT @GovChristie: The State Division of Consumer Affairs will look closely at any and all complaints about alleged price gouging.

When there’s a natural disaster some people, like Gov. Christie, start complaining in knee-jerk fashion about price gouging. And then some other people, with their knees jerking in exactly the same fashion, start complaining about people who complain about price gouging. The latter sets of knees usually belong to economists.

Suppose that an unexpected shock has occurred which has two effects. First, it increases demand for, say bottled water. Second, it cuts off supply lines so that in the short-run the quantity of bottled water in the relevant location is fixed at Q. A basic principle of economics is that if you wish to maximize total surplus then you should allow the price to adjust to its market-clearing level. This ensures that those Q consumers with the highest value for water get it. The total surplus will then be the sum of all their values.

The price plays two roles in this process, one crucial to the result, one just incidental and not necessarily intended. First, it separates out the high-value consumers from the low-value consumers. That’s the crucial role. Unavoidably it also plays a second role of taking some of that total surplus away from the consumers and giving it to producers. If you are maximizing total surplus you are completely indifferent to that second effect.

But what if you don’t want to maximize total surplus but just want to maximize consumers’ surplus? Your goal is that the Q bottles of water you’ve got should generate the greatest possible benefit for those who will consume them. I would bet that most people who understand the previous paragraph also assume that it applies equally well to the problem of maximizing consumer’s surplus. How else would you maximize it but to ensure that those with the highest value get the water?

But in fact it is quite typical for the consumer surplus maximizing solution to be a rationing system with a price below market clearing. I devoted a series of posts to this point last year. The basic idea is that the efficiency gains you get from separating the high-values from the low-values can be more than offset by the high prices necessary to achieve that and the corresponding loss of consumer surplus.

Why would we only care about consumers’ surplus and not also the surplus that goes to producers? We normally we care about producer’s surplus because that’s what gives producers an incentive to produce in the first place. But remember that a natural disaster has occurred. It wasn’t expected. Production already happened. Whatever we decide to do when that unexpected event occurs will have no effect on production decisions. We get a freebie chance to maximize consumer’s surplus without negative incentive effects on producers. And just at the time when we really care about the surplus of bottled water consumers!

Of course there are other good reasons to be skeptical of rationing in practice. It might not be enforceable, it might lead to inefficient rent-seeking, etc. But these objections mean that the debate should be about rationing in practice. The theoretical argument against it is weaker than many people think.

Yes, Boldrin and Levine keep saying the same thing over and over again, but they sure get better and better at saying it:

If a well-designed patent system would serve the intended purpose, why recommend abolishihg it? Why not, instead, reform it? To answer the question we need to investigate the political economy of patents: why has the political system resulted in the patent system we have? Our argument is that it cannot be otherwise: the “optimal” patent system that a benevolent dictator would design and implement is not of this world and it is pointless to advocate it as, by doing so, one only offers an intellectual fig-leaf to the patent system we actually have, which is horribly broken. It is fine to recommend reform but, if politics make it impossible to accomplish that reform, if they make it inevitable that if we have a patent system it will fail, then abolition – preferably by constitutional means as was the case in Switzerland and the Netherlands prior to the late 19th century – is the proper solution and proposals of reform are doomed to fail. This logic of political economy brings us to the view that we should work toward a progressive dismantlement of the patent system.

Read the article here.

A new joint paper with Alex Frankel and Emir Kamenica. The talk begins with tennis, the discussion of American Idol begins at 12:14, how to write a mystery novel is at 15:51, the M. Night Shamyalan dilemma is at 17:32, the ESPN Classic dilemma is at 18:50, and the optimal sporting contest is at 28:37.

Some time ago I had half-written a post calling for a Nobel prize for Al Roth. It was after he gave his Nancy Schwartz lecture at Kellogg and I decided not to publish it because I thought maybe it was just a little too soon. Not too soon to get the prize but too soon to expect the Nobel folks to give it to him. I am glad I was wrong.

Don’t forget his very important co-authors Tayfun Sonmez, Attila Abdulkadiroglu, and Utku Unver. These guys, Tayfun especially, were still working on matching theory when nobody else was interested and before all the practical applications (mainly coming out of their collaboration with Al) started to attract attention.

This is a time for microeconomics to celebrate. When you are on a plane and you tell the person next to you that you’re an economist, they ask you about interest rates. Everyone instinctively equates economics with macroeconomics. And that’s probably because most people have the impression that macroeconomics is where economists have the biggest impact.

But actually microeconomic theory has already had a bigger impact on your life that macroeconomic theory ever will. And there’s no politics tangled up in microeconomics. When you meet a microeconomic theorist it never once occurs to you to check the saline content of their nearest body of water.

There are no fundamental disagreements about basic principles of microeconomics. And I would say that Al Roth epitomizes what’s great about microeconomics. He has no “field:” he does classical game theory/bargaining theory and he does behavioral economics. He does theory and experiments. He theorizes about market design and he actually designs markets.

Al is the second blogger to win a Nobel prize. Compare their fields and their blogs.

I never met Shapley and I only saw him give a couple talks when he was already way past his prime. But gappy3000 reminds me that he and John Nash invented a game called Fuck Your Buddy. So that’s something. And now he has a Nobel Prize. And of course without his work there would be no prize for Roth either. David Gale should have shared the prize but he died a few years ago.

Temporary parking sign spotted near the Stanford GSB/Economics department by Michael Ostrovsky (via Google+)

On the definitions of Pareto efficiency and surplus maximization and their connection. I have also updated my slides for this lecture, presenting things in a different order in a way that I think makes a bigger impact. You can find them here.

[vimeo 50833662 w=500&h=280]Read Gary Shteyngart’s painfully comic post-mortem following a surreal transatlantic flight on American Airlines:

At Heathrow, fire trucks met us because we landed “heavy,” i.e., still full of fuel we never got to spend over the Atlantic. At the terminal, a woman in a spiffy red American Airlines blazer was sent to greet us. But the language she spoke — Martian — was not easily understood, versed as we were in Spanish, English, Russian and Urdu.

Using her Martian language skills, the American Airlines woman proposed to take us “through the border” at Heathrow, for a night of rest before we resumed our journey the next morning. An apocalyptic scenario: an employee of the world’s worst airline assigned to the world’s worst border crossing at the world’s worst airport.

The Martian took us to one immigration lane, which promptly closed. Then another, with the same result. A third, ditto. Despite her blazer, the Martian was obviously not the ally we had made her out to be. So, ducking under security ropes, knocking some down entirely, we rushed the border with our passports held aloft, proclaiming ourselves the citizens of a fading superpower.

There seems to be something going on at American Airlines. As a part of bankruptcy proceedings they are trying to get concessions from the pilot’s union. The pilots appear to have found a clever way to fight back: obey the letter of the contract and in so doing violate its spirit with extreme prejudice:

Long story short, American is totally screwed. What management is discovering right now is that formal contracts can’t fully specify what it is that “doing your job properly” constitutes for an airline pilot. The smooth operation of an airline requires the active cooperation of skilled pilots who are capable of judging when it does and doesn’t make sense to request new parts and who conduct themselves in the spirit of wanting the airline to succeed. By having the judge throw out the pilots’ contract, the airline has totally lost faith with its pilots and has no ability to run the airline properly. It’s still perfectly safe, but if your goal is to get to your destination on time, you simply can’t fly American. The airline is writing checks it can’t cash when it tells you when your flights will be taking off and landing.

Taqiyah tap: Mallesh Pai