You are currently browsing the category archive for the ‘Uncategorized’ category.

My colleagues are multi-talented:

HT: Bob McDonald for telling me first song is also by Dave Edmunds.

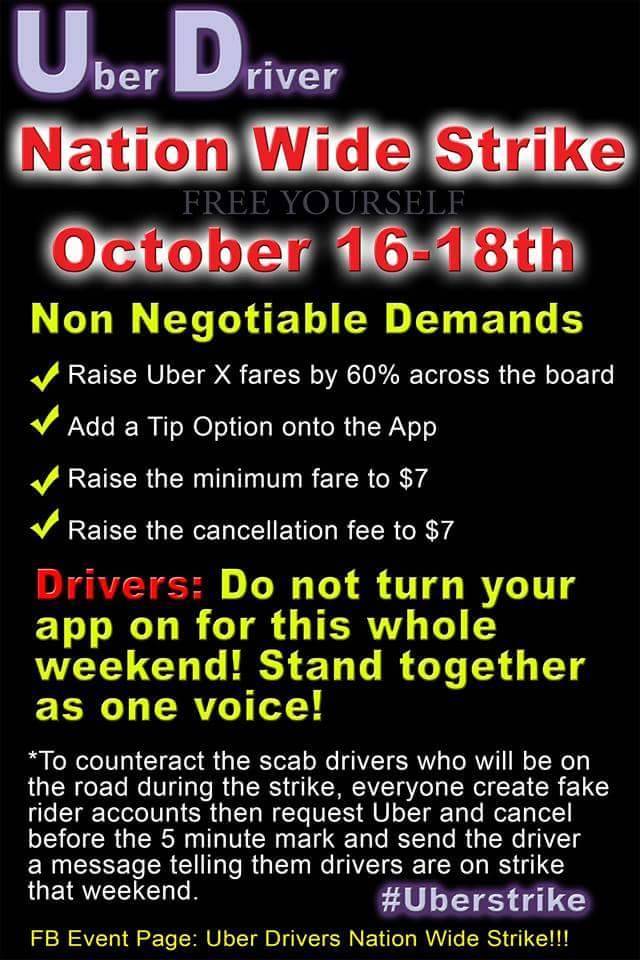

Uber Drivers tried to organize a strike to demand higher pay.

Uber drivers are competing with each for fares. The smaller the number of other drivers on the road, the greater the chance a driver get business. Also, when demand for rides outstrips supply of drivers, Uber might activate surge pricing to increase supply. Not only does a driver stand to get more business, he gets a higher fare/mile. The incentives to deviate from the strike are huge.

So, in Chicago, during the supposed strike, the number of Uber Drivers on the road was huge. Surge pricing was not activated because it was not necessary.

HT: An Uber driver.

I was on Chicago Tonight very briefly discussing Purple Pricing (see around 4 minute mark).

In 2008, the New South Wales government announced plans to build a coal mine here, promising jobs and cheap power. The coal business was booming because of demand from China. The government bought up 177 square miles of land for the mine project, boarding up 114 farms and homes.

Since then, coal prices have plummeted to their lowest level in years and the government has not been able to find a mining company willing to open a mine here. In 2013, the government abandoned its plans to develop the mine and last December appointed Goldman Sachs to sell the land.

By then, the district had lost 95 families, about 10 percent of its population. A sense of loss pervades the town, and residents feel blindsided by forces beyond their control.

Party A steals something of value to Party B and demands a ransom for its return. But once the ransom has been paid, what is to stop Party A from coming back and demanding more?

One mechanism that purchases commitment is reputation. Party A has more ransoms to extract in the future and seeks to be seen as a fair player despite being an extortionist. An interesting example is provided by Cryptowall. This “company” sends an email with a devious attachment, a virus that encrypts your harddrive if you click on it. They demand a ransom in Bitcoin to send the decryption key. The price changes over time.

The fact that they do not take your data means that they cannot come back and demand another ransom for the same data if you pay.

Because the price changes, there can be errors – you pay a ransom of 500 and by that time the price has gone up to 550 and you do not get the decryption key. What to do? A good credit card company would waive a late fee to keep a good reputation and so does Cryptowall. From the New York Times:

Use the CryptoWall message interface to tell the criminals exactly what happened. Be honest, in other words.

So she did. She explained that the virus had struck the same week that a major snowstorm hit Massachusetts and the Thanksgiving holiday shut down the banks. She told them about the unexpected Bitcoin shortfall and about dispatching her daughter to the Coin Cafe A.T.M. at the 11th hour. She swore she had really, really tried not to miss their deadline. And then a weird thing happened: Her decryption key arrived.

(HT: Alex Wearn)

You are debating a point with a colleague. Your colleague is wrong but to prove they are wrong you have to use information you know but cannot share. So, you leave things unsaid. Of course, someone who does not know the facts would also leave things unsaid by definition.

The listener knows that silence either conveys the fact that something is known but cannot be said or that nothing is known. Their inference takes the fact that you might know something but cannot say it into account. They should give you the benefit of the doubt. The benefit depends on how likely you are to know things that cannot be said. Hence, if the person leaving things unsaid is senior to the listener, the listener might defer to the speaker. Hence, seniority leads to authority via the inference content from leaving things unsaid.

“I consider that a man’s brain originally is like a little empty attic, and you have to stock it with such furniture as you choose. A fool takes in all the lumber of every sort that he comes across, so that the knowledge which might be useful to him gets crowded out, or at best is jumbled up with a lot of other things so that he has a difficulty in laying his hands upon it. Now the skillful workman is very careful indeed as to what he takes into his brain-attic. He will have nothing but the tools which may help him in doing his work, but of these he has a large assortment, and all in the most perfect order. It is a mistake to think that that little room has elastic walls and can distend to any extent. Depend upon it there comes a time when for every addition of knowledge you forget something that you knew before. It is of the highest importance, therefore, not to have useless facts elbowing out the useful ones.”

A GrAgreement has been semi-signed. Originally, the Eurozone/Germany has offered two debt relief plans for Greece.

Under Plan A, Greece votes on a number of structural reforms and puts E50blln of assets in a privatization fund in return for more bailout money and possible debt relief. Assets are sold off to recapitalize the banks.

Under Plan B, they get a time-out from the Euro and debt relief. Plan B is unpopular with the majority of voters in Greece as they want to stay in the Euro but may actually be better economically depending on the terms. (Will the EC, ECB and IMF actively help to create the new currency and give humanitarian aid? What are the terms of the debt relief?)

But both plans have significant risk: Plan A involves more austerity, declining GDP, Greek Groundhog Day and probably eventual Grexit; Plan B causes the banks to collapse unless the Troika comes up with some active help.

A better plan is variation on Plan B, if you will a Plan G: Germany should leave the Euro. Deutschit will not cause a bank run in Germany as the mark will be strong and no depositors are at risk from a haircut. The Euro will devalue helping not only Greece but Portugal, Spain, Italy, Ireland and Finland. The New Eurozone can bail out Greece and give debt relief. Germany will not have to participate in any of this and this avoids one of the main political problems domestically. There is an economic downside for Germany: the mark will appreciate so exports will be more expensive. But imports will be cheaper so there is less inflationary pressure. Plus Grexit would cause some appreciation of the Euro anyway so even Plan B has that implication.

The main problem with Plan G is it appears to signal the end of the Eurozone. This is a blow to Merkel’s record as Chancellor. But Deutschit makes the rest of the Eurozone stronger as they can deal with the the overvaluation of their common currency. Plan A, Plan B and European economic performance post-2008 already demonstrate that monetary union without political and fiscal union does not work. In fact, Deutschit signals that Germany will take a somewhat costly action to help fellow EC members. It is more likely to stabilize the Eurozone than the other options. It is success for Europe if Deutschit occurs not a failure. Once the New Eurozone has stabilized, Germany can rejoin. Of course, it will have to meet fiscal targets to be accepted by the New Eurozone including Greece. If Germany can’t return because they carry too much debt, that would both be eironikos and cause for epichairekakia (schadenfreude).

Greece and the Troika are engaged in a war of attrition. The player with the higher cost to staying IN vs conceding and dropping OUT is in a stronger position in a war of attrition.

Greece has capital controls, is about to renege on a payment to the IMF, faces an offer from the Troika that is impossible for the Greek government to get through Parliament and the offer consigns the Greeks to more austerity and economic stagnation. They have little to lose from staying IN.

The IMF does not face an existential crisis if it sticks to its guns. The EC suffers from staying IN if there is contagion but they have protected themselves.

So both sides have low costs to staying IN. They have to increases costs on the other side to persuade them to concede.

For the Troika, the strategy is straightforward: they can’t accede to the Greek request to extend the bailout for the referendum, give extra money to banks etc. This is basically what they are already doing.

For the Greeks, the strategy is more surreal: To inflict maximum cost of the Troika, Greece should default on its payments but remain in the Eurozone. Greece is cut off from international lenders anyway and the default will not have any incremental effect on their ability to borrow. With Greece insolvent, the ECB will be the key decision-maker. Do they keep on lending to Greece as they are still technically in the Eurozone? The German Finance Minister says this is the case (via Bloomberg):

German Finance Minister Wolfgang Schaeuble told lawmakers in Berlin that Greece would stay in the euro for the time being if Greek voters reject austerity in a referendum scheduled this week, according to three people present.

Schaeuble also said the European Central Bank would do what’s needed to protect the euro if Greeks voted against the bailout terms in the July 5 referendum

This is ideal for Greece. They keep the Euro and get the debt restructuring they want via default. And other countries in the Eurozone are infected by Greece being in the Euro. If Greece needs anything from the EC, this is an ideal threat point for them.

What if the ECB denies Greece credit? This state of affairs may need to be maintained by the Greek government issuing GrEuros as a medium of exchange. GrEuros can be used to pay the government as if they were Euros. GrEuros will not be accepted outside Greece by wary investors but they would trade internally in Greece. The GrEuro/Euro exchange rate will float. There is less risk of contagion here as GrEuros are not the same as Euros. Eventually GrEuros will become drachmas.

All these tactics will prolong the war of attrition. They will mask the bigger problem: How sustainable is the Eurozone with a monetary union but no political union?

I found this discussion paper by Stergios Skaperdas offered a useful perspective on the crisis. Here is a passage on default:

If Greece had defaulted in early 2010 Greek debt could have become sustainable in the long run with a writeoffs imposed on bondholders of considerably below 50% of total debt. The country would have had to borrow internally, perhaps issue IOUs (as it has done already), and impose a few modest cuts. The effect of such a policy would have been mildly recessionary.

What was done in 2010 instead by the troika was to provide Greece with loans so as to cover its budget deficit without default, in exchange for increasingly draconian budget cuts, tax increases, and institutional changes of dubious value. The effect of this policy was a fast downward spiral of the economy. Since debt kept increasing and the country kept getting poorer fast, debt was becoming ever less sustainable. Thus, the second bailout in 2012 restructured Greek debt, with the main losers being Greek pension funds and Greek banks. The Greek state had to borrow 50 billion euros just to recapitalize the banking system and continues to have to cover the losses of the pension funds (in addition to cutting pensions, cutting health expenditures, and increasing retirement ages). The continued contraction of the economy, deflation, and a few additional loans from official sources have brought the debt-to-GDP ratio close to 180%, the highest it has ever been.

Now, default would be considerably more difficult both because Greek public debt is under English law and because 80 percent of it is official and owed to official sources (the IMF, the ECB, and other Eurozone member countries). Yet, that debt is unsustainable and there is virtually no chance it will be fully paid back. Default is still a taboo but it is bound to occur in one way or another, regardless of how it is named.

Cato Unbound is running a discussion with this topic. Alex Tabarrok and Tyler Cowen kicked things off by suggesting that technological advances are ending asymmetric information as an important feature of markets. My response, “Let’s Hope Not” was just published. Josh Gans and Shirley Svorny are also contributing.

Suppose there are two bakeries which make wedding cakes and other baked items. The pastries from one bakery are pretty much the same as those from another so the baked goods market is quite competitive and margins and profits are thin.

The legislature passes a law allowing businesses to select which customers they will serve and which they will not.

One bakery, bakery A, decides to be selective and the other, bakery B, decides to be non-selective. The fact that bakery A has become selective becomes public knowledge either because the bakery advertises this fact or through word-of-mouth.

Does economic competition eliminate discrimination? This is the question.

Customers who abhor bakery A’s selection criterion boycott bakery A even if in other respects it would be convenient to just get a doughnut from bakery A. So, bakery B, gets additional business it did not get before.

Surely bakery A is suffering and hence should drop its ill-advised selection policy? Not so fast.

Some customers favor bakery A’s policy and they actively seek out bakery A’s products (the “Chick-fil-A” effect). So bakery A loses some customers but gains others. Moreover, the customers it gains are more loyal than the customers who enjoyed its products before it adopted its policy. Similarly, the customers bakery B gains are more loyal too.

Hence, product differentiation has increased because of bakery A’s active adoption of its policy and from bakery B’s decision not to adopt the same policy. The logic of competition now implies both bakeries will make more profits than they did before.

So, discrimination is not driven out by competition between firms. If anything it is reinforced by competition. This stands in contrast to Becker’s model where competition decreases discrimination in employment. (There is some way to make these models consistent by having workers have preferences over co-workers. Maybe someone already did this model?)

Without political or legal intervention, competition will not drive out discrimination.

You recently did a tour with $20 tickets and $4 beers. Is it your goal going forward to keep it affordable? Yeah. Even if you’re not a big fan, you’re like: “Let’s find something to do tonight. It’s $20 to see Kid Rock. I like one of his songs, whatever!” The scary part is, you’re going to find out who your audience is, very fast. If nobody comes for $20, it’s about time to hang the hat up.

Another reason why companies do not cut prices when demand tanks? They are worried about what they will find out about themselves. If you keep the price high and no-one buys, you can console yourself that sales would have been high if you had cut the price. If your price is low and no-one shows up, it is harder to rationalize that your product is popular.

Saudi Arabia has been trying to pressure PresidentVladimir V. Putin of Russia to abandon his support for President Bashar al-Assad of Syria, using its dominance of the global oil markets at a time when the Russian government is reeling from the effects of plummeting oil prices…Saudi officials say — and they have told the United States — that they think they have some leverage over Mr. Putin because of their ability to reduce the supply of oil and possibly drive up prices.

There is one countervailing effect that has been foreseen and dismisssed:

American and Arab officials said that even if Russia were to abandon Mr. Assad, the Syrian president would still have his most generous benefactor, Iran. Iranian aid to the Syrian government has been one of the principal reasons that Mr. Assad has been able to hold power as other autocrats in the Middle East have been deposed.

And as a major oil producer, Iran would benefit if Saudi Arabia helped push up oil prices as part of a bargain with Russia…..

But the military aid that Russia provides to Syria is different enough from what Damascus receives from Iran, its other major supplier, that if “Russia withdrew all military support, I don’t think the Syrian Army could function,” a senior Obama administration official said.

But there is a bigger one: Iran has a nuclear program that the US (and Saudi Arabia?) would like to undermine. Low oil prices and sanctions are the stick that the US has been using to get Iran to the negotiating table. An increase in the price of oil price takes away the stick etc etc. Hope the absence of any mention of this in article does not imply someone is not thinking it through.

Here are the prices you see if you access the Kiwi Rail website from Chrome in the US:

Note the blank space between the trip name and the prices. What could be there? Google “Kiwi Rail discounts” and find information that suggests accessing the Kiwi Rail website via a browser with a New Zealand IP address. When you do that, you find:

Why are people physically in New Zealand getting better deals? You can tell a demand elasticity story: New Zealanders have cars and access the website from browsers with NZ IP addresses. Their demand is more elastic than that of foreign tourists. So, price lower to people buying from NZ. You can tell the reverse story: Many tourists in NZ buy when there. Their outside option is flying and buying flights late is expensive. Tourists make up the vast majority of train travellers in NZ. People buying from abroad are also tourists but they are buying early and can find cheaper domestic flights. So their demand is elastic.So price high for people buying from NZ IP addresses but low for people buying from foreign IP addresses.

Whatever the truth of the matter, it is quite interesting to see this kind of price discrimination by Kiwi Rail. God knows what Amazon is doing in comparison!

Here is an article on the latest Michelin stars for Chicago Restaurants. The very nice thing about this article is that it tells you which restaurants just missed getting a star. As of yesterday you would have preferred the now-starred restaurants over the now-snubbed restaurants. But probably as of today that preference is reversed.

Any punishment designed for deterrence is based on the following calculation. The potential criminal weighs the benefit of the crime against the cost, where the cost is equal to the probability of being caught multiplied by the punishment if caught.

Taking surveillance technology as given, the punishment is set in order to calibrate the right-hand-side of that comparison. Optimally, the expected punishment equals the marginal social cost of the crime so that crimes whose marginal social cost outweighs the marginal benefit are deterred.

When technology allows improved surveillance, the law does not adjust automatically to keep the right-hand side constant. Indeed there is a ratchet effect in criminal law: penalties never go down.

So we naturally hate increased surveillance, even those of us who would welcome it in a first-best world where punishments adjust along with technology.

Even for the airline industry, cheaper oil may not be all good, analysts say, if carriers see it as an opportunity to increase capacity and then lower fares to fill empty seats, some analysts say. Hunter Keay of Wolfe Research LLC recently noted that airlines did just that during a previous oil slump in 2010. “Then oil prices went right back up again, as they tend to, and 2011 stunk,” he wrote.

Paul Krugman has an op-ed today where he argues Amazon is abusing its power:

Which brings us back to the key question. Don’t tell me that Amazon is giving consumers what they want, or that it has earned its position. What matters is whether it has too much power, and is abusing that power. Well, it does, and it is.

Amazon is attempting to negotiate lower prices from the publisher Hachette and is slowing down sales of Hachette books on amazon.com in an attempt to force their hand. This is the main evidence.

But this kind of bargaining leads to lower prices for consumers not higher. Hence, from the perspective of welfare it is actually good. It is akin to the argument for reducing double marginalization via vertical integration. Double marginalization occurs because the primary producer (here Hachette) and the retailer (here Amazon) BOTH add a margin on to costs to maximize profits. Welfare would be higher and prices lower if they vertically integrated so some externalities are internalized. In fact, here is Krugman in 2000 explaining why breaking up Microsoft into Windows and Office is a bad idea:

In the last few days the Justice Department, outraged by the lack of contrition among Microsoft executives, has apparently decided to seek a ”horizontal” breakup of the software company — that is, to split it into one company that sells the Windows operating system (the upstream castle) and another that sells Microsoft Office and other applications (the downstream castle)….

even if you believe that Bill Gates has broken the law, you don’t want to impose a punishment that hurts the general public. And even strong critics of Microsoft have worried that a horizontal breakup would have a perverse effect: the now ”naked” operating-system company would abandon its traditional pricing restraint and use its still formidable monopoly power to charge much more. And at the same time applications software that now comes free would also start to carry hefty price tags.

As we know from ECON 101, integration is just one way to internalize externalities. Another would be for the retailer to negotiate lower prices from the producer so they are closer to production costs. Another would be for the producer to force the retailer to charge a lower margin. As both sides try to negotiate such deals which are good for them but bad for the other side, there is a war of attrition as we see currently. Sure Amazon’s tactics may be a bit crude but this is the typical kind of negotiation that lowers input costs and eventually prices. Hachette’s tactics are harder to observe but I would bet they are not so different.

(Update Oct 21: Spelled out some more details!)

Norway and Liberia (somewhat) internalize externalities:

Norway will give Liberia up to a hundred and fifty million dollars in aid, in exchange for which Liberia will work to stop the rapid destruction of its trees.

Liberia has much of what remains of West Africa’s rain forest, but logging is rampant. The initiative is not an act of charity but a trade: Liberia gets income, which it needs; Norway gets to preserve biodiversity and take a small step against climate change. A similar deal that Norway struck with Brazil years ago helped slow deforestation there. Economists call arrangements of this kind “payments for ecosystem services,” and they follow a rationale known as the Coase theorem. In 1960, the economist Ronald Coase argued that bargaining between parties could, under certain conditions, produce a mutually beneficial and efficient solution to problems like pollution.

Brazil and US subvert efficiency via transfers:

When the WTO’s Appellate Body upheld Brazil’s claim that U.S. cotton subsidies were depressing world prices and hurting Brazilian cotton farmers in the process, the United States did not amend its subsidies to make them compliant. Rather, it agreed to pay Brazil $147 million a year for the privilege of continuing to subsidize its own farmers in a WTO-inconsistent way. This week, the United States reached another settlement, buying Brazil’s peace once more, this time to the tune of a $300 million lump sum payment.

Jean Tirole gave the Nancy Schwartz Lecture at Kellogg in 2012. He won the Nemmers Prize at Northwestern in 2014 and will be visiting in Spring 2015. So, there is no surprise that he won the Nobel Prize in Economics – it was just a matter of when, not if.

The first thing to note is that Tirole won this prize alone (though the way the advanced information is written, it leads you to think Jean-Jacques Laffont would have won the prize too if he were still alive). Most Nobel prizes are shared by two or more recipients. When it is given to just one person, it is a signal that they dominate a field. Jean Tirole dominates the field of Industrial Organization. Part of the reason for this is his textbook from 1988 which is still the best thing out there. Most people who do research just want to describe their own ideas. They go to the effort of saying why their ideas are original – otherwise the papers would be rejected by journals! But most of us stop there. Jean Tirole not only has many ideas but he can show how they fit within a broader framework. Moreover, he can describe how others’ ideas also fit together even when he not written on the topic. This is a special skill many of us do not have.

As an example, take one of his papers with Drew Fudenberg, The Fat-Cat Effect…..Along with a fundamental paper by Bulow, Geanakoplos and Klemperer, Multimarket Oligopoly…, it is the mainstay of many of the more advanced courses in Competitive Strategy in business schools. The Nobel write-up focuses on public policy, but Tirole has also had impact on private policy!

For example, think of a firm thinking of entering a market with an incumbent with a cost advantage. What’s to stop the incumbent from wiping the entrant out? Well, the entrant should be “soft” and enter with a low capacity and low price. Then the incumbent would have cannibalize high volume, high margin sales to regain a small market share. So why bother? Fudenberg and Tirole call this the puppy dog ploy. It is called Judo Economics by Gelman and Salop. It was later popularized for a business school audience. Of course, there are other circumstances where you want to look “tough” and the Fudenberg-Tirole papers tell you when you should do that – the optimal strategy is contingent on the underlying game. In fact, many, many ideas in IO can be synthesized in this framework and Chapter 8 of Tirole’s textbook shows you how.

This is just one of his many papers. In fact the Nemmers conference will focus on asset market bubbles because Tirole has made fundamental contributions in that area!

Finally, Tirole is one of the reasons why my letters of recommendation are so bad. He is student of my advisor, Eric Maskin. Eric’s letters must say “Sandeep is my 95th best student”. If it were not for Jean, I would be 94th.

Suppose there’s a precedent that people don’t like. A case comes up and they are debating whether the precedent applies. Often the most effective way to argue against it is to cite previous cases where the precedent was applied and argue that the present case is different.

In order to maximally differentiate the current case they will exaggerate how appropriate the precedent was to the specific details of the previous case, even though they disagree with the precedent in principle because that case was already decided and nothing can be done about that now.

The long run effect of this is to solidify those cases as being good examples where the precedent applies and thereby solidify the precedent itself.

Several weeks ago, I happened to pick up a bottle of Tinto Cao at Perman Wine Selections off Randolph in Chicago. The aroma made it seem like a regular New World wine – lots of fruit. But the taste was totally dry. I found more bottles at Vinic in Evanston and the first impression was reinforced in multiple bottles. Well worth the $25 – quality is comparable to much more expensive wines. The grape is Portugese but transplanted to California in the deep, dark pre-prohibition past. And when you read the back story of the winemaker Matthew Rorick and the origin of the name of label, you can’t help but be intrigued.

I’m going to a conference in New Zealand in January and just bought tickets. Just before you fly you can participate in an auction to move up one class in seats:

Using OneUp is really simple. If it’s at least seven days before your flight, go online to the OneUp page and follow the step-by-step process:

- Decide what you’re willing to offer

- Submit your offer

- Provide your payment details – you can pay by credit card, debit card or by using your Airpoints Dollars™*

- Check your offer and then submit.

When I fly, I expect the flight to be near empty so I just want to hit the reserve price. Wonder what it is?

“It’s a simple logic, bigger is better,” said Ulrik Sanders, global head of the shipping practice at Boston Consulting, “if you can fill it.”

“There’s too much capacity in the market and that drives down prices,” he continued. “From an industry perspective, it doesn’t make any sense. But from an individual company perspective, it makes a lot of sense. It’s a very tricky thing.”

Every few years, a fad comes along that takes the business world by storm. Jack Welch loved Six Sigma, others look for “synergies”, “core competencies”, “blue sky strategies”, etc etc. These fads usually involve over-generalization from a key example or set of examples.

Occasionally, a nay-sayer identifies the over-generalization. Jill Lepore has an article in the New Yorker that goes further by debunking even some of the key examples that underlie the theory of “disruptive innovation” of Clayton Christensen. What is disruptive innovation? Lepore describes it thus:

Manufacturers of mainframe computers made good decisions about making and selling mainframe computers and devising important refinements to them in their R. & D. departments—“sustaining innovations,” Christensen called them—but, busy pleasing their mainframe customers, one tinker at a time, they missed what an entirely untapped customer wanted, personal computers, the market for which was created by what Christensen called “disruptive innovation”: the selling of a cheaper, poorer-quality product that initially reaches less profitable customers but eventually takes over and devours an entire industry.

Another key example for Christensen is the disk-drive industry. Lepore follows the key companies and concludes:

As striking as the disruption in the disk-drive industry seemed in the nineteen-eighties, more striking, from the vantage of history, are the continuities. Christensen argues that incumbents in the disk-drive industry were regularly destroyed by newcomers. But today, after much consolidation, the divisions that dominate the industry are divisions that led the market in the nineteen-eighties. (In some instances, what shifted was their ownership: I.B.M. sold its hard-disk division to Hitachi, which later sold its division to Western Digital.) In the longer term, victory in the disk-drive industry appears to have gone to the manufacturers that were good at incremental improvements, whether or not they were the first to market the disruptive new format. Companies that were quick to release a new product but not skilled at tinkering have tended to flame out.

Josh Gans finds the Lepore takedown to be easy pickins’ and also does a great job explaining why Christensen’s attempt to make his theory predictive contradicted the essence of his own argument. While the takedown does not surprise Gans, it irritates the tech community:

@pmarca: What does Jill Lepore PhD in American Studies from Yale think about Bayesian algorithmic filtering?

To which I replied: “What does Clayton Christensen DBA at Harvard know about ….?” In other words, both are equally qualified/unqualified to discuss innovation. Also, why not attack Lepore’s argument not her?

But I have my own bone to pick with disruptive innovation. Let’s say an incumbent firm has a great product and buys into the disruptive innovation idea. What should it do? Since its core product is under threat of disruption, it seems the company should disrupt it themselves and invest in all sorts of technologies that look weak right now but might improve dramatically. But this does not make any sense because it implies huge costs but with little expected gain because most crappy-looking initial ideas do in fact end up on the shelf. On the other hand not investing opens up the company to disruption. To make the theory operational, we need to understand the tradeoffs. For that, you need a toy model of some sort.

The obvious candidate for such a model is Ken Arrow’s (1962?) idea of the “replacement effect” (this term was coined by Tirole). (We teach related material in our MECN 441 Competitive Strategy elective.) The profits from a new invention that supersedes the incumbent’s old product will replace the profits from the old product. Hence, the bigger the profits from the old product, the smaller are the incentives to innovate. You would destroy your own profits so no need to make the better Rice Crispy when the exisiting one is doing great. Past success rationally constrains incentives for future innovation. This theory would predict that incumbents innovate less than entrants who have no exisiting profit flow to replace. Bit like Christensen’s theory, no? Arrow pre-disrupted Christensen’s main thesis but based on rational choice analysis and with a coherent argument for assessing new investments (roughly, compare the expected NPV of current product with expected NPV of new one minus cost of investment).

As MOOCs come along, Christensen’s employer HBS has to decide how to proceed. The tradeoff is is clear and quite similar to Arrow’s point:

Universities across the country are wrestling with the same question — call it the educator’s quandary — of whether to plunge into the rapidly growing realm of online teaching, at the risk of devaluing the on-campus education for which students pay tens of thousands of dollars, or to stand pat at the risk of being left behind.

Ironically, HBS has decided not to side with Christensen but with Porter who sees no major disruption:

“Do it cheap and simple,” Professor Christensen says. “Get it out there.”

But Harvard Business School’s online education program is not cheap, simple, or open. It could be said that the school opted for the Porter theory. Called HBX, the program will make its debut on June 11 and has its own admissions office. Instead of attacking the school’s traditional M.B.A. and executive education programs — which produced revenue of $108 million and $146 million in 2013 — it aims to create an entirely new segment of business education: the pre-M.B.A.

Ed O’Bannon’s anti-trust suit against the NCAA moves forward today. Roger Noll of Stanford is likely to testify on his behalf. Here is a sample of his views from a related case:

[R]esearch in the economics of sports concluded long ago that the only way to achieve competitive parity among schools was to randomly allocate athletes and coaches among teams and prohibit athletes and coaches from switching after they have been allocated. With an unfettered competitive market for coaches and freedom of choice among student-athletes, the expected result is that the colleges with the most revenue will hire the best coaches and build the best facilities, and that as a result they will attract the best student-athletes. Interestingly, a market for student-athletes actually could improve competitive balance. If teams can pay different amounts to different students, a lesser school may find that it is willing to pay more for its first five-star athlete than Alabama or USC is willing to pay for its tenth five-star athlete. If so, the lesser schools could be somewhat more successful than they are now in recruiting top players. But even in the best of circumstances, as long as coaches and athletes have a choice, the colleges with the most to spend will have the best teams. The main effect of the scholarship limits in comparison to a market allocation is to transfer wealth from studentathletes to expenditures on coaches and facilities.

Full testimony can be found here.

These are my thoughts and not those of Northwestern University, Northwestern Athletics, the Northwestern football team, nor of the Northwestern football players.

- As usual, the emergence of a unionization movement is the symptom of a problem rather than the cause. Also as usual, a union is likely to only make the problem worse.

- From a strategic point of view the NCAA has made a huge blunder in not making a few pre-emptive moves that would have removed all of the political momentum this movement might eventually have. Few in the general public are ever going to get behind the idea of paying college athletes. Many however will support the idea of giving college athletes long-term health insurance and guaranteeing scholarships to players who can no longer play due to injury. Eventually the NCAA will concede on at least those two dimensions. Waiting to be forced into it by a union or the threat of a union will only lead to a situation which is far worse for the NCAA in the long run.

- The personalities of Kain Colter and Northwestern football add to the interest in the case because as Rodger Sherman points out Northwestern treats its athletes better than just about any other university and Kain Colter is on record saying he loves Northwestern and his coaches. But these developments are bigger than the individuals involved. They stem from economic forces that were going to come to a head sooner or later anyway.

- Before taking sides, take the following line of thought for a spin. If today the NCAA lifted restrictions on player compensation, tomorrow all major athletic programs and their players would mutually, voluntarily enter into agreements where players were paid in some form or another in return for their commitment to the team. We know this because those programs are trying hard to do exactly that every single year. We call those efforts recruiting violations.

- Once that is understood it is clear that to support the NCAA’s position is to support restricting trade that its member schools and student athletes reveal year after year that they want very much. When you hear that universities oppose removing those restrictions you understand that whey they really oppose is removing those restrictions for their opponents. In other words, the NCAA is imposing a collusive arrangement because the NCAA has a claim to a significant portion of the rents from collusion.

- Therefore, in order to take a principled position against these developments you must point to some externality that makes this the exceptional case where collusion is justified.

- For sure, “Everyone will lose interest in college athletics once the players become true professionals” is a valid argument along these lines. Indeed it is easy to write down a model where paying players destroys the sport and yet the only equilibrium is all teams pay their players and the sport is destroyed.

- However, the statement in quotes above is almost surely false. Professional sports are pretty popular. And anyway this kind of argument is usually just a way to avoid thinking seriously about tradeoffs and incremental changes. For example, how many would lose interest in college athletics if tomorrow football players were given a 1% stake in total revenue from the sale of tickets to see them play?

- My summary of all this would be that there are clearly desirable compromises that could be found but the more entrenched the parties get the smaller will be the benefits of those compromises when they eventually, inevitably, happen.

Quite disturbing even though you know no volts are coursing through the subject’s body.